Nope.

Fine, but why?

Let’s start with banking as it used to be

Over a century ago, before the Fed, before FDR, and before all the monetary shenanigans, this was money:

We made it through the industrial revolution without all this debt nonsense, and we did so in a way where costs were constant for generations. Gold and silver worked as money.

Greenbacks

Gold and silver are heavy though – paper is easier to transact in, and paper and metal currency was interchangeable. It was a lot easier to buy real estate with a stack of these than with the equivalent (1.7 pounds each!) gold coins:

Banking

Prior to the Fed, banking worked like this:

- You put your money in the bank

- The bank would pay you interest on the money you kept there

- This interest was earned from investing in government and corporate debt (for savings banks), or by issuing loans to the community (reference the Bank Run scene from It’s a Wonderful Life).

- The interest you receive on your account was less than the interest earned from investing your assets, but that was the business model.

This presents a problem with human nature, though: the more you loaned out the more interest your clients (and your bank) would make, but the greater the chance a bank run would happen. There were reserve requirements in place to insure a minimum store of money was kept, but these could be quite low – in 1917 it was as low as 3% on some kinds of deposits.

So sometimes the progression would work like this:

- Banks keep high reserve ratios. This is safe, but it comes with a lower return for the bank, and for savers.

- Eventually, some banks assume riskier reserve ratios and/or take on riskier investments. This results in a higher return for the bank, and as a result savers can be paid a higher interest rate.

- Since most people see banks as essentially the same and interchangeable, savers would migrate from the safer banks to the banks paying higher interest. As a result, more banks had to assume higher risk profiles, or be bought out by banks that did.

- All this happened in economic ‘good times.’ Once things start to head downward, more savers need to withdraw their savings, and corporate and consumer loans start to fail at a higher rate.

- This reduces trust in banks, and enough people withdraw their funds that the bank becomes insolvent, and people lose savings (see the movie clip linked above).

The Fed was implemented to be a lender of last resort to these distressed banks, but it went on to become that entity we all know and love now.

Now, back to Kinesis

Kinesis is comparable to how this generalized model of how money used to work, with some protections built in:

- Kinesis vaults gold and silver like banks used to, but instead of storage receipts like greenbacks Kinesis tracks ownership on a blockchain. This means you can spend your vaulted gold on a debit card, or directly to another person, on seconds, anywhere in the world.

- Kinesis has a 100% reserve ratio – every gram on the blockchain is matched by a gram in the vaults. It’s one thing to say this, but it’s another to pay one of the oldest 3rd party vault auditors to verify your holdings on a regular schedule, then publish the results. Audits haven’t be as regular as expected with Covid, but in 2023 they are happening quarterly. Every audit performed has shown there is enough metal vaulted to cover every gram on the blockchain – something no competitor in this space can come close to.

- Instead of buying bonds, making loans, or loaning out your assets for a return, Kinesis derives its yields from transfer fees. This is at the core of the model – Kinesis makes money from the movement of money, and the word Kinesis is derived from the Greek word for movement.

So with Kinesis we know every gram of gold and silver is in the vaults, and we can see that the yields come from use of the system. Yields are currently low, but as the system grows (and two nation states are in the process of implementing Kinesis as the machinery behind national payment systems) yields will scale up proportionally.

Now, on to ‘Paper Gold’

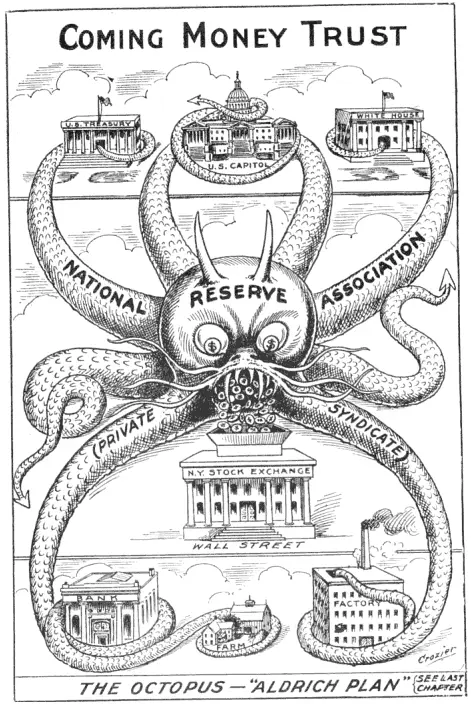

There is a lot of chicanery seems to be going on with the COMEX, LBMA, and LME – the big institutions where precious metals are traded, and the source of current pricing for the metals. In these cases banks and large players can buy and sell “gold” and “silver” in huge quantities – we’ve seen sales in 5 minutes that represented months of real silver production in the real world, far in excess of the amount of vaulted silver that could be used to fill these orders. But these orders aren’t about buying and selling in a traditional sense – this is a game that’s settled in cash at the end of the every month. SchiffGold estimates that there are 17.4 paper ounces of silver for each registered ounce in the COMEX, and Chris Marcus made the point that there may be 500 claims on every ounce of silver that’s in existence.

When I hear “paper gold” this is what I think about – COMEX contracts for the purchase of silver that simply doesn’t exist in the COMEX Registered vaults. This is market manipulation mostly, and if someone were to buy a few contracts for delivery that will probably find them impossible to deliver.

The we come to products like SLV and GLD, run by Blackrock, which trade the same way index funds do on stock exchanges. Investors buy these to get exposure to the gold and silver prices, but this is about short-term trades or volatility reduction strategies more than it is about buying the physical metals.

There is a strong suspicion that these vehicles are not backed by the metal that is supposed to back each share, and some of the movement we do see shows that entities that get caught shorting metal on the COMEX and are forced to deliver appear to use these funds as sources of deliverable metal. Regardless, people with normal means are not capable of taking possession of the metal that’s supposed to back these trusts.

The difference between Kinesis and “paper gold”

There are meaningful differences:

- Buying Kinesis coins means you’re buying legal title to metal in vaults that you know exists, because the audits prove it. There is no such proof for SLV and GLD, and the proof shows that COMEX is hugely over-leveraged. If you want to own gold and silver and have someone else vault it, you can do so with confidence when using Kinesis.

- Kinesis metal is deliverable. Often, Kinesis is the cheapest form of delivery. The minimums to do so are 200 ounces of silver or 100 grams of gold ($4,378 and $5,993 as I type this), and this costs an additional 0.45%, plus $100 and the actual cost of delivery. For the minimum silver delivery, figure about 8% above the spot price which is cheaper than buying from a dealer online. COMEX, SLV, and GLD are just about impossible for a regular person to take delivery from.

What about counter-party risk?

Kinesis is a counter-party. That’s why I think about Kinesis more as a replacement for financial services, and as a supplement to my physical stack. This brings me to my next point though: diversification is important.

In these last few years we’ve seen some worldwide crises. Think back – you’ve seen the footage of Ukrainian families leaving the nation, Syrian refugees fleeing war or recovering from the most recent earthquake, and so on. Touching images, and in each case what we see are:

- Family units

- On foot

- Most carrying nothing but the clothes on their back.

- The luckiest carrying a rolling travel bag that will be searched by authorities.

I’d like to imagine two scenarios. You’re a reasonable stacker, and you have 4 monster boxes accumulated.

- In the first case, you have all 4 monster boxes in your safe.

- In the second case, you’ve got 2 monster boxes in your safe, and 1000 KAG stored in Kinesis.

Now, you wake up tomorrow and need to leave, now. As in, pick your kids up from school, put them in the car, and go without delay. When you run out of gas, you’ll walk until you reach safety. Forest fires, train wrecks releasing phosgene gas, war, famine, hurricane, earthquake — I don’t care, pick one.

Now, put yourself in the place of those refugees. Are you going to carry 4 monster boxes (130 lbs of metal) across a border, into a tent city surrounded by desperation and poverty, and use that stored wealth to get a fresh start? Or is that going to disappear in 4 days, because carrying your 4 year old is more important than the metal, or it’s seized at a checkpoint, or simply taken by people more desperate than you?

Now, what about that 1,000 ounces in Kinesis? You can have it delivered once you get to your final destination, which is nice. You can also use the Kinesis debit card to book yourself a hotel with good food and a shower instead of going into a camp. When the physical debit card is released again you can convert your metal to local currency at any ATM.

Yes, Kinesis is a counter-party. But I think the security of having your metal vaulted somewhere so it’s still yours should you be separated from your local stash is worth a lot in these uncertain times.

Kinesis is a supplement to your stack, not a replacement. It’s a replacement for some of your financial services.