We now live in a negative yielding world – the official inflation rate is over five percent, but the unofficial rate (calculated as the CPI was calculated in 1980) is over twelve percent. Ten-year Treasuries are yielding 1.35% percent, guaranteeing purchasers a minimum 4% loss of purchasing power every year. Using the Treasury’s official numbers, “inflation adjusted” treasuries are even losing 1.85% of their real value every year! Investors in need of yield have been pushed to riskier and riskier bonds, and as a result even junk bonds now have a negative yield.

Everywhere you look, prices are going up and buying power is being inflated away. The only exceptions to this seem to be the unbacked crypto-currencies, property values, and the stock market, which is still pushing for all-time-highs.

If you aren’t comfortable betting on Ethereum or Bitcoin (or their volatility isn’t suitable for your all of your savings), and you know better than to make big bets on stock and housing markets when they are at their all-time highs, then what are your alternatives?

I’d like to present the one I’ve settled on personally – Kinesis

Kinesis is Sound Money

Kinesis is an old idea, updated for the digital age, and built with an incentive structure that gives it a real future. Conceptually it’s easy to understand (it’s a distributed ledger that tracks physical assets), but it takes a while to get your head wrapped all of the implications of the system.

The Status Quo

Right now we keep our money in bank accounts as a digital record, and when we spend it we either use cash we get from ATMs, or (increasingly) we purchase using a card, via the VISA or Mastercard network. The costs for VISA and Mastercard result in overall costs that are 1.5% to 3% higher, but we don’t seem to mind the increase because of the convenience this offers. We are apparently happy to pay 3% more in order to get 1% of that back, and pay up to 28% on our credit card balance if we don’t pay it off in full and on time every month.

If the Internet goes down, our ability to pay (or withdraw money) goes down. This is a rare occurrence, and it’s frustrating, but we accept it.

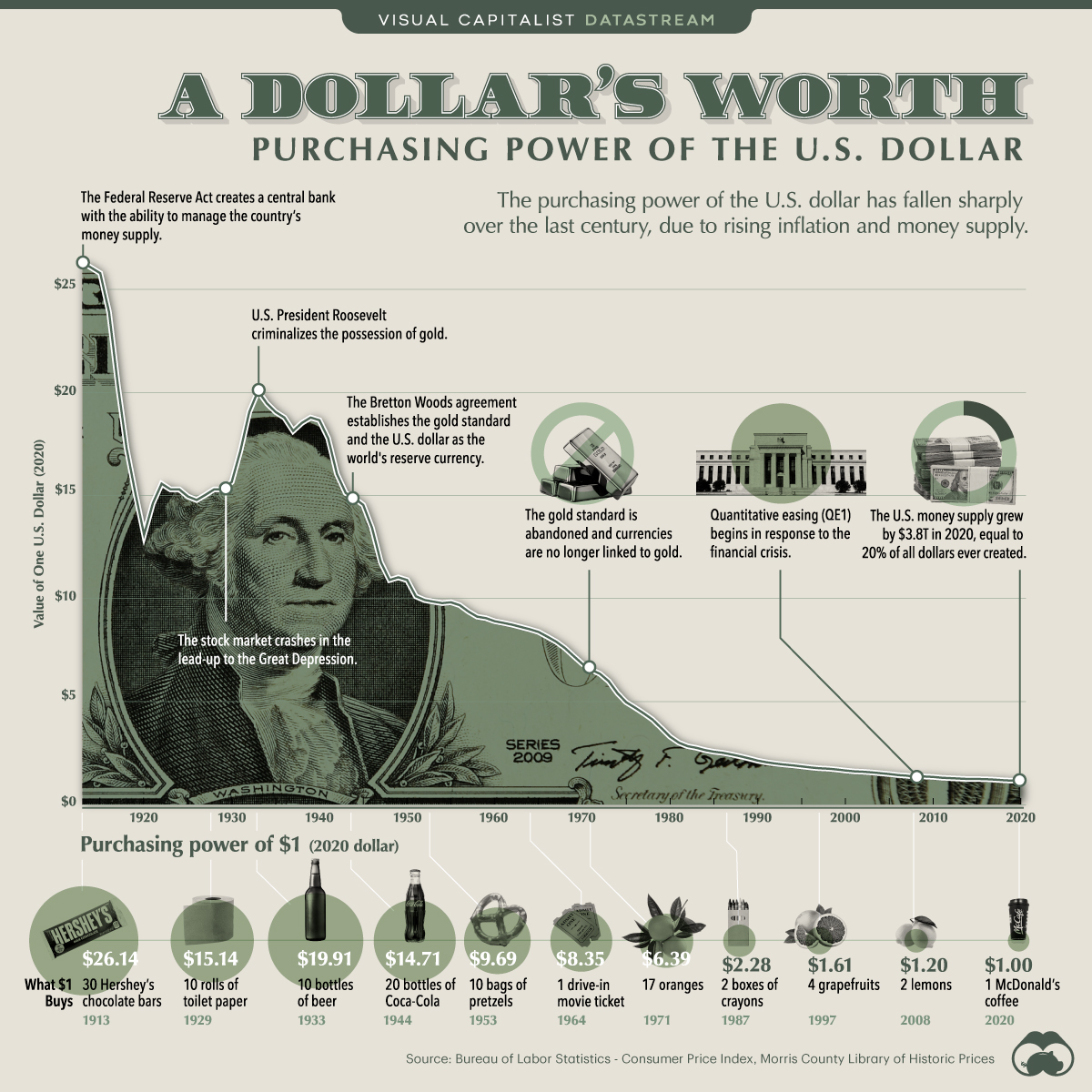

Backing all of this system is the US Dollar which has lost 96% of its purchasing power since 1971. The Dollar is the World Reserve Currency, and nobody really seems to think about the slow loss of wealth that represents.

Now, enter Kinesis

Kinesis aims to be a better money.

- Kinesis Protects Against Inflation. Instead of using dollars as the money within the system, Kinesis uses gold and silver, which historically have been among the best stores of wealth and purchasing power during inflationary and uncertain times. If gold and silver continue to keep up with inflation, then transferring your dollars into Kinesis KAU and KAG should result in a hidden 5.4% to 12% annual increase in purchasing power versus dollars (depending on which CPI measure you favor.)

- Kinesis Lowers Transaction Costs. The distributed ledger assesses fees on transfers automatically. The most expensive transfer in Kinesis is from wallet to wallet, and these transfers only cost 0.45%. If I send you $100 (or buy a $100 item) I pay $0.45 for the transfer. This is much cheaper than credit cards, though the sender pays the fee rather than the recipient. It is significantly cheaper than services like Western Union.

- Kinesis Can Be Used In the Real World: You can spend it in the real world, via a VISA debit card. Topping up the card costs 0.22%, so adding $100 to your card costs you an additional $0.22. If you have a physical Kinesis debit card you can withdraw up to $920 daily from ATMs.

- Kinesis gives users yields on their gold and silver assets, based on user fees rather than leasing or anything risky. This is transformational, and is something that simply wasn’t possible before the blockchain was invented.

- Kinesis is Sharia Compliant. This doesn’t matter for most first-world users, but since Kinesis does not charge interest, it has a real chance to take off in areas of the world where traditional banking still is not used. Like Indonesia.

- You Can Withdraw Your Money At Any Time. It costs $100 plus shipping and insurance to have your gold or silver delivered to you, and this can be done in quantities as low as 100 grams of gold, or 200 ounces of silver. Overall rates to do so are generally lower with Kinesis than with traditional gold and silver retailers. If you prefer you can link your bank account, sell your KAU and KAG on the exchange, and simply transfer the proceeds to your bank account electronically.

- There are no storage fees. Lots of places will vault your gold and silver. None will do so without charging for the service. Except Kinesis.

How it Works

At its base, Kinesis is twelve vaults in eight countries, fully insured, audited twice annually by a third party, and managed by Brinks, Loomis, and Malca-Amit. For those familiar with the terminology, Kinesis offers allocated, pooled storage — the audits guarantee that the total amount of gold and silver in the system exactly match the coins on the blockchain, but users have ownership of their respective number of ounces in the vaults, and not individual bars.

To track ownership down to the 100,000th of a gram/ounce and allow for simple transfers, Kinesis modified the Stellar blockchain. This allows Kinesis to processes transfers in 1-3 seconds and scale up to greater than the annual average volume of the VISA network while maintaining that performance level.

Gold and silver in the vaults belong to the users of the system – Kinesis has a bailee relationship with it’s users – and Kinesis moved its headquarters to Lichtenstein after the laws in Lichtenstein were updated to recognize the blockchain as a legal record of ownership. Should Kinesis fail, our gold and silver are still held in our names, and while it would be frustrating to have to deal with Brinks and Loomis to get it delivered, it’s not gone. (I only emphasize this because previous attempts at merging gold and the blockchain sometimes failed because the company running the program could take out loans against the assets they were securing, as they were on the books as an asset of the company. This is not possible with Kinesis, by design. We own the metal; we don’t just have claims against a corporation’s assets. This is important.)

Breaking it down Conceptually

The easiest way to get your head wrapped around Kinesis’ model is to start from zero and build up.

So, let’s imagine Kinesis with zero assets in the system. There are no KAU (digital gold) or KAG (digital silver) in the system, but the vaults are running, the distributed ledger is up, the VISA debit card is there, and the market maker is sitting in the background waiting to make markets.

- First, you transfer money into Kinesis by wire transfer, or using Wise, or some other method. This is still the weakest part of Kinesis, as it can be hard to get your money into the system.

- Once your dollars (or Euros, or Pounds) have been received by Kinesis, you can now mint KAU or KAG. This process starts with buying gold 100 grams at a time (or silver at 200 ounces at a time) from the market maker, generally at something around 0.3% over the spot price. In return the coins you just minted (100 KAU or 200 KAG) are deposited in your Kinesis account, and the bars you purchased are moved into Kinesis’ vault. Let’s say you minted 1,000 KAG.

- At this point, there are 1,000 KAG in the system, all in your wallet. You can load this onto your VISA debit card, or place them for sale on the Exchange so other users who want to buy KAG in exchange for dollars, or pounds, or bitcoin can do so. Let’s say you offer 500 of these for sale in the Exchange.

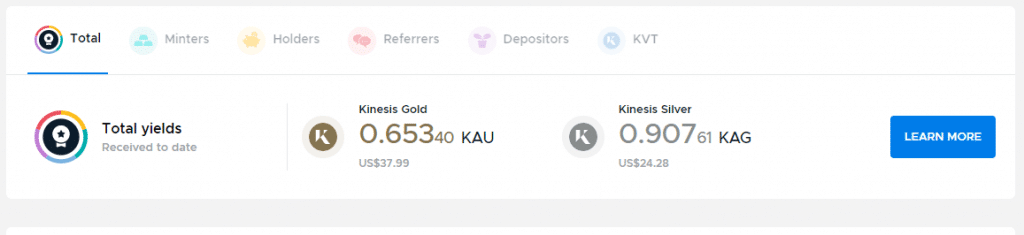

- Now, I come along and I can’t mint 200 KAG at a time because it’s too expensive, so I buy 50 KAG from you. Since the 50 KAG you minted have now left your wallet and been released into the system, those KAG are now eligible for the minter’s yield. Minter’s yield is a yield paid to the minter, in gold and silver, every month, in perpetuity. This is an incentive for regular folks to create the KAU and KAG that Kinesis needs to function. Remember – Kinesis owns none of the assets in the system, so the base metal backing KAU and KAG needs to come from somewhere. That comes from minting.

- Now, I have 50 KAG, you have 500 KAG, and we will assume other buyers have purchased the remaining 450 KAG that you sold on the market. Each day we hold those coins in our wallets, we qualify for the holder’s yield. This gives gold and silver a yield for the first time in history, and incentivizes people to make their gold and silver purchases on Kinesis.

Now it’s time to talk about yields.

As mentioned above everything done on Kinesis incurs a small fee. Buying or selling on the Exchange costs 0.22%, topping up your VISA card costs 0.22%, sending to others costs 0.45%. These fees go into what Kinesis calls the master fee pool, and this pool is then redistributed to the participants in the Kinesis system. Kinesis itself is the authoritative source on yields, and they have a great series of short videos that describe the system, but the summary is here:

All the fees generated go into the master fee pool, which is distributed every month. 52.5% of the total fees paid out go to the users of the system:

- 5% of the total fees are divided among the minters. This is the minter’s yield.

- 15% of the total fees go to those who held metals in the system, proportionally. This is the holder’s yield.

- 7.5% of the fees go to the folks who referred their friends into the system. That’s 7.5% of the total fees your friend pays, forever. So if you sign up with this link I’ll get credit for your sign-up. When you spend $100, $0.45 is added to the fee pool, and I get 3.38 pennies of that. It’s not much, but hopefully you’ll spend lots of money via Kinesis.

- 5% of the fee pool goes to the depositor’s yield, which is essentially the amount of KAU and KAG you purchased in the first two weeks after funding your account. This is a minter’s yield equivalent for those who can’t transfer in $6,000 at a time, and it encourages people to jump in with both feet, helping grow the system faster.

- 20% of the total fee pool is divided among the people who own KVT. There are only 300,000 KVT that will ever exist, and these were initially sold to give Kinesis the start-up capital they needed to build the platform. Some other were rewards for minters, and others bought these as investments.

The remainder of the fees are distributed as follows:

- Kinesis gets 17.5%. This covers the cost of the system, and hopefully generates a profit.

- Partners like Indonesia get 20% of the fees their users generate, so as 200 million un/under-banked Indonesians start saving and spending via Kinesis, Indonesia is building their national gold stockpile fractions of a gram at a time, funded with every transaction Indonesians make.

- White label functionality will be available in the future, and companies that white-label Kinesis get 10% of the yields their users generate.

The CEO of Kinesis has also mentioned a spender’s yield as something to be introduced in the future, but the implementation is still unclear.

The Reality: Kinesis Today

Right now there are market-makers who are making money insuring spreads are tight on the Exchange. Yesterday the buy/sell spread on an ounce of silver (KAG) was $0.18, which isn’t bad at all. If metals within Kinesis are currently more expensive than on the physical market, then the market makers mint more coins. If the costs are cheaper on Kinesis than on the physical market, then the market maker redeems their holding for physical. Market makers are exempt from the transfer costs we pay, and are also ineligible for yields, but their existence means the market price we see for digital gold and silver is always extremely close to what the physical market price is.

This means that if you think that silver has more up-side than gold (like I do), you can buy KAG now, wait for the prices to move to a more appropriate level, then easily and quickly change your silver for gold when it’s time to move out of silver again. No haggling at the coin shop, no negotiating, or carrying it for the transfer, or worrying if what you’re receiving is gold-plated tungsten – just a simple transaction on the web interface or from the app. Simple, and at a fair price.

If you want to redeem your KAG or KAU for physical, it’s easy. You pay $100 plus shipping and insurance, and your metals are delivered to you, from the Kinesis vault closest to you. A user on Reddit did this during the silver squeeze earlier this year and paid 8.17% above spot all-in for his two 100 ounce bars. That’s about the best price that was available anywhere on the world.

All is not perfect, however. Currently, Kinesis is still exiting its startup phase, and there are some growing pains:

- It is still difficult to get your money into the system. Wires are expensive and complicated, so most people use wise.com for low cost transfers into Kinesis. This needs to get easier.

- I have a physical VISA debit card that works, and I used to have a virtual card, but no longer. Kinesis opted to move from their debit card provider to a new one and there have been delays related to Covid and the move to Lichtenstein. The physical cards are only currently available in the US, though they are set to roll out in the UK and EU later this year. With the loss of the virtual cards, the spending has dropped, and the resulting yield has decreased as well. This will be fixed soon, but there’s no transparency here.

- Audits require all vaults to be audited simultaneously, some of the vaults are in Australia, and nobody is allowed to travel to Australia due to Covid lock-downs, so the current audit is late. This will be performed…when Australia allows it. It may be a while.

- The Indonesian collaboration is built, and should really fuel the yields Kinesis generates, but it hasn’t been announced. Indonesia was hit hard by Covid, and the announcement was delayed as a result. Earlier this week the lock-downs officially ended, however, so I hope we see the Indonesia announcement (and the resulting flow of up to 200 million un-banked Indonesians into Kinesis) soon, but it’s been a waiting game.

- The minter’s yield went live last month, and other yields are being accrued, but no other yields are yet being paid. They should all be online by the end of the year, but they aren’t here yet. This also means some of the implementation details are still guesswork.

I think Kinesis is The Best Money

Inflation is here, appears to not be transitory, and looks to be increasing.

Kinesis is sound money that can be used for saving in gold and silver, and for day-to-day spending, and for payments and transfers to real people via e-mail, app, or text message. Things aren’t perfect yet, but I think the model is exceptional and I expect great things moving forward.

I’d encourage you to give it a shot. I’m enthusiastic enough that I built this site to try and simplify things for newer members. If you want to try it out, I’d appreciate it if you used my referral link when you sign up – why let Kinesis keep that money when it could go to a referrer instead?